Georgia Foreclosure Timeline 2026: What Every Atlanta Homeowner Needs to Know Before It’s Too Late

Quick Answer: Georgia’s foreclosure timeline typically runs 60 to 180 days from the first missed payment to a completed courthouse steps sale. Georgia is a non-judicial foreclosure state — lenders do not need court approval to foreclose. The sale takes place on the first Tuesday of each month at the county courthouse. Homeowners have no right of redemption after a non-judicial foreclosure sale in Georgia. Federal rules generally prohibit foreclosure from beginning before 120 days of delinquency — but once that clock expires, the process can move in as few as 37 days.

Georgia has one of the fastest foreclosure timelines in the United States. From the first missed payment to a completed courthouse steps auction, the entire process can move in as few as 60 days — with no court involvement, no judge, and no second chance once the gavel falls.

That is not an exaggeration written to alarm you. It is the legal reality of living in a non-judicial foreclosure state. And in Atlanta’s real estate market, where median home values are approaching $300,000 and rising, a foreclosure is not just a housing threat — it is a wealth destruction event. Homeowners with $100,000, $150,000, even $200,000 in equity are losing it at Fulton County courthouse steps auctions every year because they didn’t fully understand the Georgia foreclosure timeline they were already inside.

This guide covers everything Atlanta homeowners need to know about the 2026 Georgia foreclosure timeline: what makes Georgia unique, the full stage-by-stage process, your legal rights at each step, what has changed in 2026, and the five realistic options available to you depending on where in the timeline you currently are. Read this before you need it. If you already need it, read it now.

What Makes Georgia’s Foreclosure Timeline Different From Other States

Georgia is one of approximately 27 non-judicial foreclosure states in the United States — meaning lenders can foreclose on a property entirely outside the court system. There is no lawsuit. No judge reviews the case. No court hearing gives the homeowner an opportunity to respond. The lender handles the entire process through notice and advertisement, and when that process is complete, the property is sold at public auction.

To understand what this means in practice, compare Georgia’s timeline to other major states. In Florida, a judicial foreclosure state, the average time from first missed payment to completed sale runs 6 to 18 months because the lender must file a lawsuit and proceed through the court system. In New York, also judicial, the process can run 12 to 36 months. In California, a non-judicial state, the law requires a minimum of 111 days from the Notice of Default to the auction date.

In Georgia, the minimum time from the first Notice of Sale publication to the actual auction is 37 days. The total process from first missed payment to auction — accounting for the federal 120-day protection discussed in H2 3 — typically runs 150 to 180 days when servicers follow federal guidelines. But in practice, homeowners who miss that protection window can face an auction date within weeks of understanding what is happening.

The Power of Sale Clause

Every Georgia mortgage and deed of trust contains a power of sale clause — a contractual provision that grants the lender the authority to sell the property upon default without going to court. This is the legal foundation of non-judicial foreclosure, and it is in every mortgage document signed at every closing in Georgia. When you signed your mortgage, you agreed to this clause.

No Right of Redemption After Non-Judicial Foreclosure

One of the most important and most misunderstood facts about Georgia’s foreclosure process is this: Georgia does NOT provide a statutory right of redemption after a non-judicial foreclosure sale. Once the auction is complete and the foreclosure deed is conveyed to the winning bidder, the former homeowner has no legal right to reclaim the property. This is a critical distinction from Georgia’s tax sale process, which does include a 12-month redemption period. Many homeowners confuse the two. They are entirely different legal processes with entirely different outcomes.

Fulton County foreclosure sales take place at the Fulton County Courthouse, 136 Pryor Street SW, Atlanta, GA 30303, on the first Tuesday of each month between 10:00 a.m. and 4:00 p.m. DeKalb, Cobb, Clayton, and Gwinnett County sales follow the same first-Tuesday schedule at their respective courthouses.

The Complete Georgia Foreclosure Timeline — Stage by Stage (2026)

Here is the full Georgia foreclosure timeline in clear, sequential stages with the timeframes that apply in 2026. Understanding exactly where you are in this process is the first step toward taking effective action.

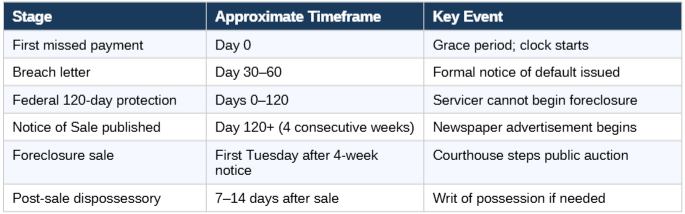

Stage 1: First Missed Payment (Day 0)

Most Georgia mortgage loans include a 15-day grace period before a late fee is assessed. After that grace period, the loan is technically in default. Most servicers don’t begin formal default proceedings until 30 or more days past due, and federal rules create a significant protection window — but the clock starts at Day 0.

Stage 2: Breach Letter / Notice of Default (Day 30–60)

After 30 to 60 days of non-payment, the servicer sends a formal breach letter — sometimes called a Notice of Default or demand letter. This document states the total amount owed to cure the default, the deadline to cure (typically 30 days), and the lender’s stated intent to accelerate the loan and proceed to foreclosure if the default is not resolved. Receipt of a breach letter is the signal that formal foreclosure proceedings are being prepared.

Stage 3: The 120-Day Federal Protection Window (Days 0–120)

Under CFPB mortgage servicing regulations, a servicer cannot make the first notice or filing required to initiate foreclosure until the borrower has been delinquent for more than 120 days. This is a federal protection that applies in Georgia regardless of how quickly state law would otherwise allow the process to proceed. It is the most important legal protection in the Georgia foreclosure timeline and creates a meaningful window for homeowners to pursue loss mitigation, refinance options, or a planned sale.

This protection is not automatic — it requires that the servicer is following federal rules. A HUD-approved housing counselor or attorney can verify compliance and flag any violations.

Stage 4: Notice of Sale Published (Day 120+)

Once the 120-day period has expired and the servicer decides to proceed, the lender must publish a Notice of Sale in the official legal organ of the county where the property is located, once a week for four consecutive weeks. In Fulton County, the official legal organ is the Daily Report. Under O.C.G.A. § 44-14-162, the notice must include the property description, sale date and location, the secured party’s name, and the amount of the debt. The lender must also send written notice to the borrower by certified mail at least 30 days before the sale date under O.C.G.A. § 44-14-162.2.

The minimum time from the first Notice of Sale publication to the auction is 37 days. Once you see your property advertised in the Daily Report, you have weeks — not months.

Stage 5: Foreclosure Sale — First Tuesday at the Courthouse

Georgia law requires foreclosure sales to take place on the first Tuesday of each month between 10:00 a.m. and 4:00 p.m. at the county courthouse. The sale is a public auction. The lender typically opens bidding at the amount of the outstanding debt. If no third-party bidder exceeds the opening bid, the lender takes the property back through a credit bid. Once the foreclosure deed is conveyed, the former homeowner has no further legal claim to the property. There is no right of redemption.

Stage 6: Post-Sale Dispossessory

After the foreclosure sale, the new owner must initiate a dispossessory proceeding in magistrate court to formally remove the former homeowner. Georgia’s dispossessory process is also fast — a writ of possession can be obtained in as few as 7 to 14 days if the former homeowner does not vacate voluntarily.

No right of redemption: Unlike Georgia’s tax sale process — which includes a 12-month redemption period — a completed non-judicial mortgage foreclosure in Georgia is final and irreversible. Once the foreclosure deed is conveyed at the courthouse steps sale, there is no legal mechanism to reclaim the property. Every option in this guide must be exercised before the auction.

Your Legal Rights During the Georgia Foreclosure Process

Most Georgia homeowners in foreclosure don’t realize they have specific, legally enforceable rights throughout the process. These rights, if understood and exercised, can significantly change the outcome.

The 120-Day Federal Rule (CFPB)

Under CFPB mortgage servicing regulations, a servicer cannot make the first notice or filing required to initiate foreclosure until the borrower has been delinquent for more than 120 days. This federal rule applies in every state, including Georgia, regardless of how fast state law otherwise allows the process to move. It creates a meaningful window — four months — during which homeowners should be actively pursuing every available option. The CFPB mortgage servicing rules protecting homeowners from foreclosure are federal regulations that apply to all servicers and are enforceable by the CFPB.

The Dual-Track Prohibition

Under the same CFPB rules, if a borrower submits a complete loss mitigation application before the servicer has made the first notice or filing for foreclosure, the servicer cannot proceed to foreclosure while that application is under active review. This is called the dual-track prohibition. Filing a complete application — not a partial one — is what triggers this protection. A HUD-approved housing counselor can help prepare a complete application and ensure the protection is properly invoked.

Right to Certified Mail Notice

O.C.G.A. § 44-14-162.2 requires the secured party to send written notice of the foreclosure sale to the borrower by certified mail at least 30 days before the sale date. If this notice is not properly sent, the foreclosure may be subject to legal challenge. Keep all certified mail notices — and if you have reason to believe a sale is pending and you have not received certified mail notice, consult a Georgia real estate attorney immediately.

Right to Cure the Default

At any point before the foreclosure sale, the homeowner can cure the default by paying the full reinstatement amount in certified funds. Georgia law allows reinstatement up to five business days before the scheduled sale date. The reinstatement amount includes all missed payments, late fees, attorney fees incurred by the lender, and the cost of the foreclosure advertisement. Get this figure directly from the servicer’s loss mitigation department in writing.

Right to Sell Before the Auction

The homeowner retains the unconditional right to sell the property at any point before the foreclosure auction. A sale that closes before the auction date stops the foreclosure, pays off the mortgage from proceeds, and preserves any remaining equity. This is the most financially important right in the entire Georgia foreclosure timeline for homeowners with equity.

Right to File Bankruptcy

Filing a bankruptcy petition triggers an automatic stay under federal law that immediately halts all collection actions, including a scheduled foreclosure sale — even on the morning of the auction. Chapter 13 allows homeowners to repay arrears over 3 to 5 years while maintaining current mortgage payments. Consult a Georgia-licensed bankruptcy attorney to determine whether this is appropriate for your specific situation.

If you have reason to believe your servicer has violated any of these federal requirements — particularly the 120-day rule or the dual-track prohibition — this is a documentable legal issue that may provide grounds to delay or challenge the foreclosure. An attorney or HUD counselor can help you assess whether violations have occurred.

What’s Changing in Georgia Foreclosure Law in 2026

Georgia’s core non-judicial foreclosure process has remained largely unchanged for decades. However, several developments in 2025 and 2026 are affecting the landscape for distressed Atlanta homeowners — and every homeowner should be aware of them.

The Georgia Senate Property Tax Relief Bill

The Georgia Senate recently passed a property tax relief bill setting up a potential showdown with the House. While not directly a foreclosure statute, rising property tax bills in Fulton County and Metro Atlanta have been a significant and growing contributor to mortgage default — homeowners managing a $4,500 or higher annual tax bill on top of a mortgage payment face compounding financial pressure that increases foreclosure vulnerability. If the bill becomes law, relief could reduce this pressure for thousands of Atlanta-area homeowners.

Post-COVID Loss Mitigation Programs Sunsetting

Several COVID-era mortgage forbearance and loss mitigation programs have sunset or are in the final stages of sunsetting as of 2026. Homeowners who entered forbearance arrangements that were not fully resolved — either through a formal repayment plan, modification, or deferral — may find themselves returning to active default status. This is creating a secondary wave of foreclosure risk for some Atlanta-area homeowners who believed their situation was settled.

CFPB Regulatory Environment

The CFPB’s regulatory posture is subject to ongoing political and legal uncertainty in 2026. The 120-day rule and the dual-track prohibition are critical federal protections for Georgia homeowners — because Georgia’s state process moves so fast, any weakening of federal protections would disproportionately affect borrowers in non-judicial states. Homeowners and housing advocates should monitor developments through the CFPB’s official regulatory updates.

Servicer Compliance Issues

Several major mortgage servicers have faced enforcement actions in recent years for failing to comply with loss mitigation requirements before proceeding to foreclosure. Georgia homeowners should know that servicer non-compliance is a real, documentable, and correctable issue. A HUD-approved housing counselor can help verify whether your servicer is following required federal procedures and flag any violations that may create grounds for delay.

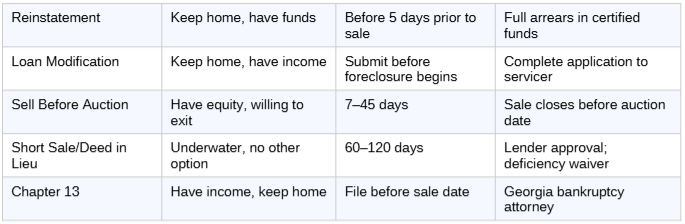

Five Options to Stop Foreclosure in Georgia Before the Auction

Every option in this list is available to you right now. None of them will exist after the courthouse steps sale. The right option depends on your equity position, your income, how far into the timeline you are, and what your goal is for the property.

Option 1: Reinstatement — Pay the Arrears

Pay everything past due in a single certified funds payment: all missed principal and interest, late fees, attorney fees, and the cost of any foreclosure advertisement. Must be paid at least five business days before the scheduled sale date. This is the cleanest solution when financially accessible — it stops the foreclosure completely, restores the original loan terms, and leaves no mark on the title.

Option 2: Loan Modification or Forbearance

Submit a complete loss mitigation application to your servicer’s loss mitigation department. A complete application triggers the CFPB’s dual-track prohibition, legally preventing the servicer from proceeding to foreclosure while the application is under review. A loan modification permanently changes the loan terms — interest rate, payment amount, or loan term — to a level the homeowner can sustain. A forbearance provides temporary relief with a structured repayment plan afterward. A free HUD-approved housing counselor can prepare and submit this application on your behalf.

Option 3: Sell Before the Auction

For homeowners with equity, this is the most wealth-preserving option in the entire Georgia foreclosure timeline. A traditional sale generates full market-rate proceeds if there is enough time — and in Metro Atlanta’s market, many homes list and close within 30 to 45 days. If the auction is closer, an as-is cash sale can close in 7 to 21 days. The mortgage arrears, attorney fees, and all liens are paid at closing from proceeds. The homeowner walks away with remaining equity instead of losing it entirely at auction. Understand your rights throughout this process with the Georgia Legal Aid homeowner rights during foreclosure guide.

Option 4: Short Sale or Deed in Lieu

For homeowners who are genuinely underwater — whose mortgage balance exceeds the property’s current value — a short sale (selling for less than the outstanding balance with lender approval) or a deed in lieu (voluntarily transferring title to the lender) may be the most realistic exit. Both require lender cooperation. Both can include a negotiated deficiency waiver. Both are less damaging to credit and less visible in public records than a completed foreclosure. Confirm any deficiency waiver in writing before closing.

Option 5: Chapter 13 Bankruptcy

Filing a Chapter 13 petition immediately halts the foreclosure through the federal automatic stay — even on the morning of the scheduled sale. Chapter 13 allows homeowners with regular income to repay mortgage arrears through a court-approved 3 to 5-year plan while maintaining current mortgage payments. It is a multi-year commitment and requires a Georgia-licensed bankruptcy attorney. It is not the right tool for everyone, but for homeowners with income who want to keep the home, it is a legally available and sometimes the most effective path.

Fulton County and Atlanta-Specific Foreclosure Resources in 2026

You do not have to navigate the Georgia foreclosure timeline alone. Here are the most important local and state resources available to Atlanta-area homeowners in 2026.

Fulton County Courthouse Foreclosure Sales — First Tuesday of each month, 136 Pryor Street SW, Atlanta, GA 30303. Sales between 10:00 a.m. and 4:00 p.m. The Daily Report publishes the list of scheduled sales — search your property address if you believe a notice may have been filed.

HUD-Approved Housing Counselors in Atlanta — Free foreclosure prevention counseling from certified agencies. HUD counselors communicate with servicers, prepare loss mitigation applications, and help homeowners understand all available options. The free HUD-approved foreclosure counselor locator for Atlanta connects you with local agencies at no cost. Atlanta-area agencies include HomeFree-USA Atlanta and the Urban League of Greater Atlanta.

Atlanta Legal Aid Society — (404) 524-5811. Free legal representation for low-income Fulton County homeowners facing foreclosure. Can challenge improper foreclosure procedures and represent homeowners in loss mitigation disputes.

Georgia Senior Legal Hotline — (404) 389-9992. Free legal advice for homeowners age 60 and older on foreclosure, property taxes, and housing matters.

Georgia Department of Law Consumer Protection Division — Accepts complaints against mortgage servicers who are not following required federal loss mitigation procedures. If your servicer has violated the 120-day rule or the dual-track prohibition, this is the state-level enforcement channel.

Georgia Department of Community Affairs — Administers state-level housing assistance programs that may include mortgage assistance for qualifying homeowners. Check current program availability directly, as programs change annually based on funding.

What Happens to Your Equity at the Courthouse Steps

This is the section most homeowners wish they had read before the auction. As a real estate consultant, I want to be as direct as possible: allowing a foreclosure to complete on a property with equity is the single most expensive mistake an Atlanta homeowner can make.

How the Auction Math Works

The lender opens bidding at the outstanding debt amount — which may be significantly less than the property’s market value. If no third-party investor bids above the opening amount, the lender takes the property back at the debt amount through a credit bid. The former homeowner receives nothing. Not the difference between the debt and the property value. Nothing.

Here is what that looks like in Fulton County’s current market: a property worth $350,000 with a $220,000 outstanding mortgage balance goes to auction. The lender opens at $220,000. No investor bids higher. The lender takes the property back. The former homeowner loses $130,000 in equity — equity they would have received had they sold before the auction — and walks away with $0. This scenario happens at Fulton County courthouse steps sales every single month.

The Deficiency Judgment Risk

After a non-judicial foreclosure in Georgia, the lender may pursue a deficiency judgment for the difference between the outstanding loan balance and the foreclosure sale price. Under O.C.G.A. § 44-14-161, a deficiency action must be filed within 30 days of the foreclosure sale confirmation. For homeowners with equity, a deficiency is unlikely because the auction proceeds typically cover the debt. For underwater homeowners, it is a real risk that compounds the damage of the foreclosure itself.

The Pre-Sale Opportunity

A homeowner who sells before the auction captures equity the auction will eliminate. In Fulton County’s current market, even a significantly discounted as-is cash sale to an investor typically results in more money than a courthouse steps auction where the lender takes the property back at the debt amount. Verify your equity position using the Fulton County Tax Commissioner’s property records portal, then calculate the difference between your property’s current market value and your outstanding mortgage balance. That gap is the equity you are protecting — or surrendering.

The homeowners who preserve their equity are the ones who act before the auction. A cash sale at a modest discount is almost always better than a courthouse steps auction that returns nothing. Time is the variable that makes this possible. Use it.

Final Thoughts: In Georgia, the Foreclosure Clock Doesn’t Wait

The Georgia foreclosure timeline is fast, final, and unforgiving to those who don’t understand it. But it is not hopeless — as long as you act before the first Tuesday auction date. The 120-day federal protection window, the right to cure, the right to sell, the dual-track prohibition — these are real and meaningful protections. But every single one of them expires the moment the courthouse steps sale is complete.

If you are reading this because you’ve already missed payments, already received a breach letter, or already seen your property in the Daily Report — your options still exist today. Make the call. Submit the application. List the property. Do something. The cost of inaction in Georgia is final and irreversible in a way that almost no other state matches.

Facing Foreclosure in Atlanta or Fulton County? Let’s Figure Out Your Options.

If you’re looking at the Georgia foreclosure timeline and recognizing where you are in it — whether you’re at the breach letter stage, watching for a Notice of Sale in the Daily Report, or already past the 120-day mark — the time to act is right now, not after the first Tuesday. I’m Gerald Harris, founder of ATL Home Help Solutions, and I work with homeowners across Fulton County and Metro Atlanta who are trying to understand their options before a courthouse steps auction takes those options away. Whether it’s understanding your equity position, figuring out the fastest path to a solution, or knowing which phone call to make first — I’m here to help.

No pressure. No judgment. Just honest guidance from someone who knows this market.

📞 Call or Text: 404-913-7086 📧 Email: gerald@atlhomehelp.com

Visit ATL Home Help Solutions — Contact Gerald Harris — No pressure. No judgment. Just honest local guidance.