What Happens If You Can’t Afford Your House Anymore in Georgia?

You’ve owned your Atlanta home for years. You’ve made every payment. And now — because of a job loss, a medical crisis, a divorce, a death in the family, or a fixed income that simply hasn’t kept pace with rising costs — you are sitting at the kitchen table staring at a mortgage bill you cannot pay. The fear is real. The shame is real. And the confusion about what happens next is real too.

But here is what matters most: you have more options than you think, and more time than you fear — but only if you act now. Georgia is a non-judicial foreclosure state, which means the foreclosure process moves significantly faster than in most other states. That single fact changes everything about how quickly you need to respond.

This guide covers what Georgia law actually says happens when you stop paying, what your real options are before foreclosure, what to do in the first 30 days, how Atlanta-specific resources can help, and how a voluntary sale compares to foreclosure for homeowners who have built real equity in this market. Whether you’ve missed one payment or received a foreclosure notice, the right information at this moment is the most valuable thing you can have.

What Georgia Law Says Happens When You Stop Paying Your Mortgage

Understanding Georgia’s foreclosure process is not optional information — it is the foundation for every decision you make from this point forward. Georgia operates under a non-judicial foreclosure system, which means the lender does not need to go to court to foreclose on your home. This single legal fact makes Georgia one of the fastest foreclosure states in the country.

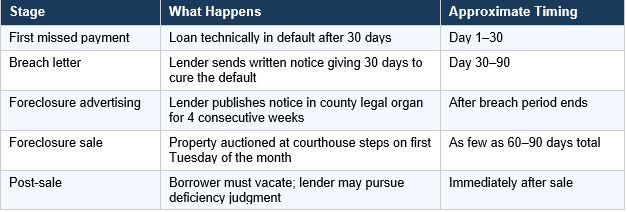

The Georgia Foreclosure Timeline

That 60-to-90-day window is not a comfortable cushion. It is an extremely tight timeline when compared to the months or years most people assume they have. In practice, many servicers do not move on the first missed payment and begin with outreach first. But waiting for that outreach is not a strategy in Georgia. The window for the best options is open the moment financial hardship begins.

What a Foreclosure Sale Means for an Atlanta Homeowner

Fulton County foreclosure sales are held at the Fulton County courthouse on the first Tuesday of each month. At the sale, the property is auctioned — the lender bids the outstanding loan balance and third parties can bid higher. The critical financial reality: foreclosure sales in Georgia typically produce below-market prices because the buyer pool is limited to cash-only bidders willing to purchase a property sight unseen. A home worth $350,000 on the open market can sell for $210,000 at a foreclosure auction. Any equity above the final sale price and foreclosure costs goes to the former homeowner — but that number is almost always dramatically lower than a voluntary market sale would have produced.

The Deficiency Judgment Risk

If the home sells at foreclosure for less than the outstanding loan balance, Georgia lenders can pursue a deficiency judgment for the difference. This means a homeowner can lose their home AND still owe money afterward. A deficiency judgment in Georgia can be collected through wage garnishment and bank account levies. This is one of the most financially devastating outcomes of foreclosure — and one of the strongest arguments for resolving the situation before the sale date.

Georgia’s foreclosure timeline is one of the fastest in the United States. A homeowner who waits for a situation to ‘work itself out’ after missing a payment may find themselves with no options left within 60 to 90 days. The first call to your servicer should happen the moment you know you cannot make a payment — not after you miss it.

The Georgia Attorney General consumer protection resources for homeowners facing foreclosure at consumer.georgia.gov covers your rights as a Georgia borrower and the legal protections available during the foreclosure process.

The First 30 Days — What You Must Do Immediately

The actions taken in the first 30 days after financial hardship begins determine which options remain available to you. Every day that passes without action narrows the field.

1. Call your loan servicer the day you know you can’t make the payment: The single most important action is the most avoided one. Most servicers have a loss mitigation department specifically to help borrowers avoid foreclosure. Federal law under the Real Estate Settlement Procedures Act requires servicers to provide information about available loss mitigation options. When you call, say exactly this: “I am experiencing financial hardship and I am concerned about my ability to make my upcoming mortgage payment. I would like to discuss all available loss mitigation options.” Document every call: date, time, representative name, and everything discussed.

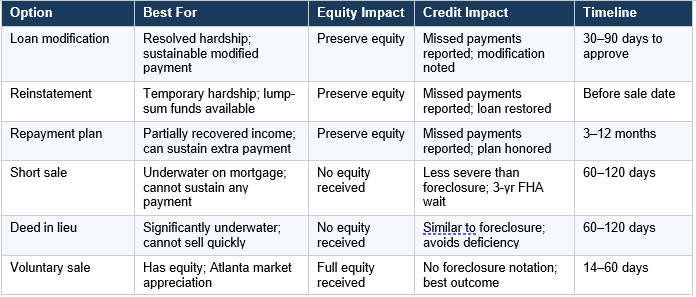

2. Request forbearance: Forbearance temporarily pauses or reduces your payments for 3 to 12 months. It is not forgiveness — the missed amounts must eventually be repaid — but it creates critical breathing room. FHA, VA, USDA, Fannie Mae, and Freddie Mac loans all have forbearance provisions. Private conventional loan borrowers should ask specifically what forbearance options are available through their specific servicer.

3. Request a loan modification simultaneously: A modification permanently changes the loan’s terms — interest rate, loan term, or both — to make the payment affordable going forward. Processing typically takes 30 to 90 days, which means applying the day hardship begins is the only way to have a decision before foreclosure proceedings potentially begin. You will need: proof of hardship, income documentation, bank statements, and a written hardship letter.

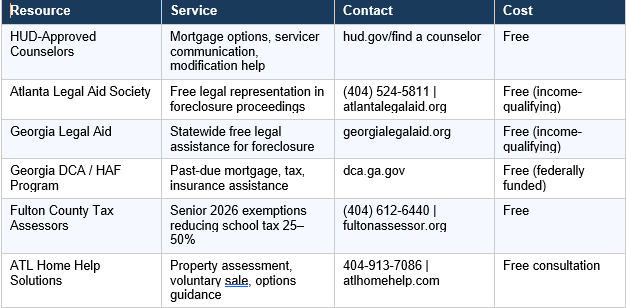

4. Contact a free HUD-approved housing counselor: HUD-approved housing counseling is completely free and specifically designed for this situation. The counselor reviews your mortgage, evaluates all available options, assists with servicer communication, and helps prepare modification applications. Find a HUD-approved counselor at the free HUD-approved foreclosure prevention counselor locator in Georgia.

5. Apply for Georgia mortgage assistance programs: Georgia’s Homeowner Assistance Fund (HAF) was federally funded to cover past-due mortgage payments, property taxes, insurance, and HOA dues for qualifying homeowners. Check current 2026 availability and application status at dca.ga.gov. Program funding status changes — verify current availability immediately.

6. What NOT to do: Do not ignore servicer letters. Do not transfer the deed to a family member to avoid foreclosure. Do not pay any company upfront fees to “save” your home. Do not stop paying property taxes and insurance even if you stop paying the mortgage — these create additional default triggers that can accelerate the process.

Your Real Options — From Loan Modification to Voluntary Sale

Once you understand Georgia’s timeline and have made initial contact with your servicer, the next question is which path forward best fits your specific situation. Here is an honest comparison of every real option available.

The Voluntary Sale — The Most Overlooked Option for Atlanta Homeowners

For Atlanta homeowners who have owned their property for 5 or more years, a voluntary sale before foreclosure is almost always the financially superior option to any form of distressed resolution. Here is why this matters so much in Atlanta’s specific market:

Metro Atlanta home values have appreciated dramatically over the past decade. A homeowner who purchased in 2010 for $180,000 and currently owes $95,000 on a home now worth $380,000 has $285,000 in equity. In a foreclosure auction, that home might sell for $220,000 — with the lender recovering their balance and the homeowner receiving whatever small surplus remains after fees. In a voluntary market sale, that $285,000 in equity — minus standard closing costs of roughly $15,000 to $20,000 — goes directly to the homeowner to fund the next chapter.

A cash buyer sale in Atlanta can close in as few as 14 to 21 days — well within Georgia’s foreclosure timeline if action is taken before the advertising period begins. This is not a distressed sale or a desperate measure: it is a financially rational decision that preserves equity that the foreclosure process would eliminate.

The equity reality in Atlanta: Most Fulton County homeowners who have owned for 5+ years are not underwater. They have real, significant equity that foreclosure will effectively erase. A voluntary sale is not giving up — it is protecting what you have built before the legal process takes it.

Foreclosure Rescue Scams Targeting Atlanta Homeowners — Know the Warning Signs

Distressed Atlanta homeowners are a primary target for foreclosure rescue scammers. Fulton County foreclosure notices are publicly filed and searchable — scammers actively monitor this data to identify and contact homeowners in default. Understanding these scams before they reach you is essential protection.

Common Scam Types Active in Metro Atlanta

• Advance fee “save your home” companies: Charge $1,500 to $5,000 or more upfront to “negotiate with your lender.” It is illegal in Georgia for a foreclosure rescue company to collect fees before performing services. These services are either identical to free HUD counseling or simply fraudulent.

• Rent-to-own rescue schemes: The scammer asks the homeowner to sign over the deed with a promise they can “rent back” and repurchase the home later. The homeowner loses the deed; the rent payments provide no path back to ownership; eviction follows.

• Phantom help: Companies collect paperwork and fees, communicate with the servicer just enough to delay foreclosure slightly, then disappear — leaving the homeowner further behind and with less time and fewer options.

• Equity stripping: A buyer offers to purchase the home at a discounted price with a leaseback option. The equity is stripped at closing and the leaseback terms are designed to fail. The homeowner loses both the home and the equity they built.

How to Identify a Legitimate vs. Fraudulent Resource

Legitimate resources: HUD-approved housing counselors (free), Atlanta Legal Aid Society (free legal help), your servicer’s own loss mitigation department, licensed Georgia real estate agents and cash buyers who provide written offers with no upfront fees.

Warning signs: upfront fees required before services are performed; pressure to sign documents quickly without review time; requests to make mortgage payments to a new account or company; promises to “stop foreclosure guaranteed.”

Report suspected scams to the Georgia Attorney General’s Consumer Protection Division at consumer.georgia.gov. Atlanta Legal Aid Society at (404) 524-5811 provides free legal assistance to qualifying homeowners victimized by foreclosure rescue fraud.

Atlanta-Specific Resources for Homeowners Who Can’t Afford Their House

Every Atlanta homeowner in financial hardship should know these resources before making any decision.

The 2026 Fulton County Senior Tax Exemptions — A Relief Tool for Fixed-Income Homeowners

For senior Atlanta homeowners whose hardship is driven by rising property taxes rather than mortgage default, the new 2026 exemptions approved by voters in November 2025 may restore affordability without requiring any sale or modification. Seniors age 65 to 69 in the Fulton County Schools district receive a 25% reduction in school tax assessed value. Those 70 and older receive a 50% reduction. City of Atlanta seniors age 65 and older receive a $50,000 reduction in assessed value for Atlanta Public Schools taxes.

These exemptions are applied automatically for eligible seniors who already have a basic homestead exemption on file — no new application required for most qualifying homeowners. If you have not received a postcard confirming automatic application, contact the Fulton County Board of Assessors at (404) 612-6440 or apply at fultonassessor.org before April 1. For seniors who own their home free and clear but are struggling with the tax burden alone, this exemption may be the difference between keeping and losing the home.

For guidance on all available Georgia homeowner assistance programs and current foreclosure prevention resources, the Georgia DCA homeowner assistance programs for Georgians facing foreclosure at dca.ga.gov provides current program status and application information.

Frequently Asked Questions: Can’t Afford Your House in Georgia (2026)

These are the questions Atlanta homeowners in financial hardship ask most often.

Q: How long do I have before the bank can take my house in Georgia?

Georgia is a non-judicial foreclosure state with one of the fastest foreclosure timelines in the United States. Once you miss a payment and the breach letter period has elapsed (typically 30 days), the lender can begin 4 consecutive weeks of required public notice and then schedule the foreclosure sale for the next available first Tuesday of the month. In a worst-case scenario, a Georgia homeowner can go from first missed payment to foreclosure sale in as few as 60 to 90 days. In practice, most servicers begin with outreach before moving to formal foreclosure proceedings — but waiting for that outreach is not a safe strategy. Contact your servicer the moment you know you cannot make a payment.

Q: Will I lose all my equity if my Atlanta home goes to foreclosure?

In most cases, effectively yes. Foreclosure sales in Georgia typically produce below-market prices because the buyer pool is limited to cash-only bidders at the courthouse steps. A home worth $350,000 on the open market may sell for $210,000 to $230,000 at auction. The lender recovers their loan balance first; any surplus above that goes to the former homeowner. But that surplus is almost always dramatically less than what a voluntary open-market sale would have produced. For Atlanta homeowners with significant equity, a voluntary sale before foreclosure preserves far more of what they have built.

Q: Can I sell my house if I’m behind on mortgage payments in Georgia?

Yes — and if you have equity, this is often the single best option available. You can sell your home at any point before the actual foreclosure sale date. If you need a quick sale, a cash buyer can close in as little as 14 to 21 days in Atlanta. The sale proceeds first pay off the outstanding mortgage balance including arrears, and any remaining equity goes directly to you. For Atlanta homeowners who have owned for 5 or more years in an appreciating market, a voluntary sale before foreclosure can preserve $100,000 to $400,000 or more in equity that would otherwise be lost.

Q: What is a loan modification and will it affect my credit?

A loan modification permanently changes the terms of your mortgage — typically by reducing the interest rate, extending the loan term, or both — to make the monthly payment affordable. Applying for a modification does not itself damage your credit. However, if you are behind on payments during the modification process, those missed payments do appear on your credit report. A completed modification is typically noted on your credit file as “modified,” which can affect some future lending. Working with a HUD-approved housing counselor during the modification process improves both the approval likelihood and the outcome clarity.

Q: What is the difference between forbearance and a loan modification?

Forbearance is temporary — it pauses or reduces your payments for a set period with the understanding that those amounts must eventually be repaid. It does not change your loan terms. A modification is permanent — it changes the loan’s interest rate, term, or both so that the new lower payment becomes your standard going-forward obligation. Forbearance is appropriate for short-term hardships. Modification is appropriate for long-term hardships where the original payment is no longer sustainable. Many servicers require a completed forbearance period before approving a modification.

Q: Can property tax increases cause me to lose my Atlanta home even if I have no mortgage?

Yes. In Georgia, unpaid property taxes result in a tax lien on the property. If taxes remain unpaid, the county can sell the tax lien to investors who can then pursue a tax deed process to take ownership. This is one of the most devastating housing loss scenarios in Atlanta — particularly for long-term senior homeowners in Cascade Heights, West End, and East Point who own their home free and clear but cannot sustain rising property taxes. The 2026 Fulton County senior exemptions (25% to 50% reduction for ages 65+) may restore affordability. Apply at fultonassessor.org before April 1.

Q: Are foreclosure rescue companies in Atlanta legitimate?

Most are not. It is illegal in Georgia for a foreclosure rescue company to collect upfront fees before performing services. Legitimate help — HUD counseling, Georgia Legal Aid, Atlanta Legal Aid Society — is entirely free. Any company that charges upfront fees to negotiate with your lender, asks you to sign over your deed with a promise to rent back, or guarantees to stop foreclosure is either operating illegally or fraudulently. Report suspected scams to the Georgia Attorney General’s Consumer Protection Division at consumer.georgia.gov.

Q: What should I do first if I just missed my first mortgage payment in Georgia?

Call your loan servicer immediately. Do not wait for them to contact you. Tell them you are experiencing financial hardship and request information about all available loss mitigation options, specifically forbearance and loan modification programs. While waiting for the servicer’s response, contact a free HUD-approved housing counselor at hud.gov/findacounselor who can help you navigate the process. If you have significant equity in your Atlanta home and are uncertain whether to keep or sell it, contact ATL Home Help Solutions for a free, no-pressure property assessment that gives you the full picture before you commit to any single path.

Final Thoughts: Options Exist — But Only If You Act Before Georgia’s Clock Runs Out

The question of what happens if you can’t afford your house anymore in Georgia has many possible answers — and the one you experience depends almost entirely on how quickly you act after the hardship begins. Georgia’s non-judicial foreclosure process gives lenders a fast path to a sale that can strip away decades of equity in a single courthouse auction. The homeowners who preserve the most — their credit, their equity, their options — are the ones who respond in the first 30 days, not the ones who wait for the foreclosure notice to arrive.

Whether your path forward is a modification, a forbearance, a voluntary sale, or a combination of programs and resources, the starting point is the same: make the call today. Every Atlanta homeowner in this situation deserves honest guidance, not sales pressure and not silence. The resources exist. The options exist. Use them.

Facing a Housing Crisis in Atlanta? ATL Home Help Solutions Provides Honest Guidance — No Pressure, No Judgment.

If you’re reading this because you’re facing a situation you didn’t expect and don’t know how to navigate — you are not alone, and this is not the end of the story. Atlanta homeowners in financial hardship have more options than they think. But those options narrow quickly in Georgia’s fast foreclosure environment. I’m Gerald Harris, founder of ATL Home Help Solutions. I work with Atlanta and Fulton County homeowners who are trying to protect what they’ve built — whether that means staying in the home through a modification, selling before foreclosure to preserve equity, or understanding every realistic option before making a decision that can’t be reversed.

Your home represents more than a transaction. Let’s protect what you’ve built.

📞 Call or Text: 404-913-7086 📧 Email: gerald@atlhomehelp.com

Visit ATL Home Help Solutions — atlhomehelp.com — No pressure. No judgment.